INVESTMENTS BACKED BY REAL ESTATE

Current Investment Opportunities

We help match our investors to deals that fit their timelines and budgets.

Get on our calendar to review new opportunities

NEW BUILD

Modern Two Story 3 Bed 3.5 Bath

per side Duplex built in Holmen,

WI.

FUNDED &

SOLD

NEW BUILD

4 Bedroom 3 Bathroom Home built in Holland, WI.

FUNDED &

SOLD

NEW BUILD

4bd, 3.5ba Farmhouse Design built in La Crosse, WI on Holmgren Drive.

FUNDED &

SOLD

NEW BUILD

3 Bedroom 3 Bathroom Home built in West Salem, WI.

FUNDED &

SOLD

NEW BUILD

3 Bedroom 3 Bathroom Home built in Greenfield, WI.

FUNDED &

SOLD

NEW BUILD

4 Bedroom 3 Bathroom Home built in West Salem, WI.

FUNDED &

SOLD

NEW BUILD

Modern Single Story 3 Bed 3 Bath per side Duplex being built in Holmen, WI.

FUNDED & FOR

SALE

NEW BUILD

3 Bedroom 3 Bathroom Home being built in Greenfield, WI.

FUNDED

NEW BUILD

4 Bedroom 4 Bathroom Home built in Greenfield, WI.

FUNDED & FOR

SALE

INVESTMENTS BACKED BY REAL ESTATE

Current Investment Opportunities

We help match our investors to deals that fit their timelines and budgets.

Get on our calendar to review new opportunities

NEW BUILD

Modern Two Story 3 Bed 3.5 Bath

per side Duplex built in Holmen,

WI.

FUNDED &

SOLD

NEW BUILD

4 Bedroom 3 Bathroom Home built in Holland, WI.

FUNDED &

SOLD

NEW BUILD

4bd, 3.5ba Farmhouse Design built in La Crosse, WI on Holmgren Drive.

FUNDED &

SOLD

NEW BUILD

3 Bedroom 3 Bathroom Home built in West Salem, WI.

FUNDED &

SOLD

NEW BUILD

3 Bedroom 3 Bathroom Home built in Greenfield, WI.

FUNDED &

SOLD

NEW BUILD

4 Bedroom 3 Bathroom Home built in West Salem, WI.

FUNDED &

SOLD

NEW BUILD

Modern Single Story 3 Bed 3 Bath per side Duplex being built in Holmen, WI.

FUNDED & FOR

SALE

NEW BUILD

3 Bedroom 3 Bathroom Home being built in Greenfield, WI.

FUNDED

NEW BUILD

4 Bedroom 4 Bathroom Home built in Greenfield, WI.

FUNDED & FOR

SALE

Why Do We Pay Such High Rates of Return?

This all seems too good to be true...

Why do we pay higher rates of return than everyone else, you may ask?

Then the answer is "The Need For SPEED!"

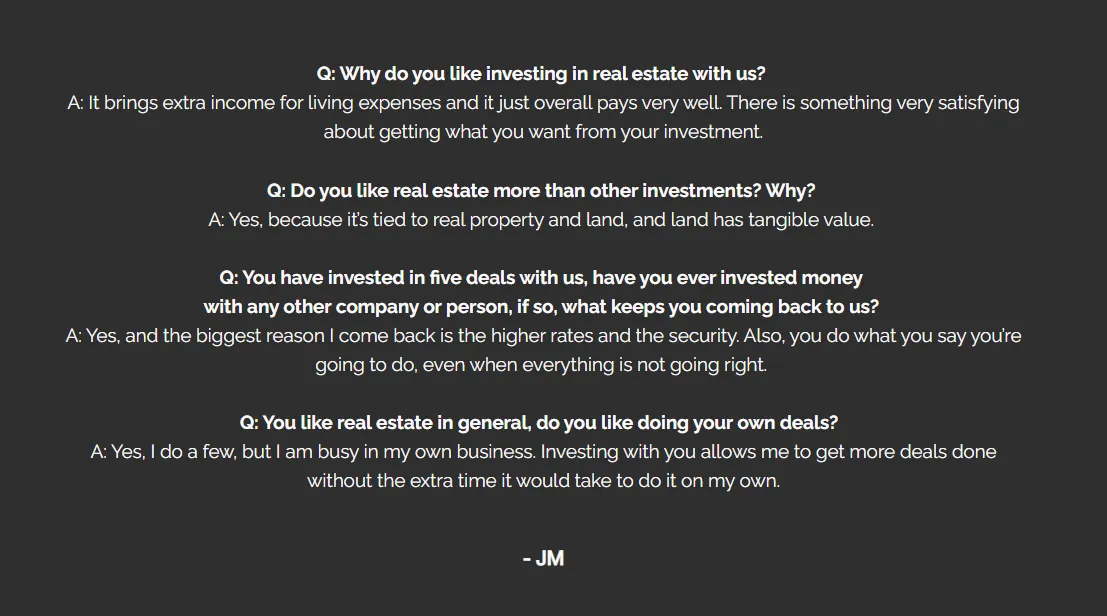

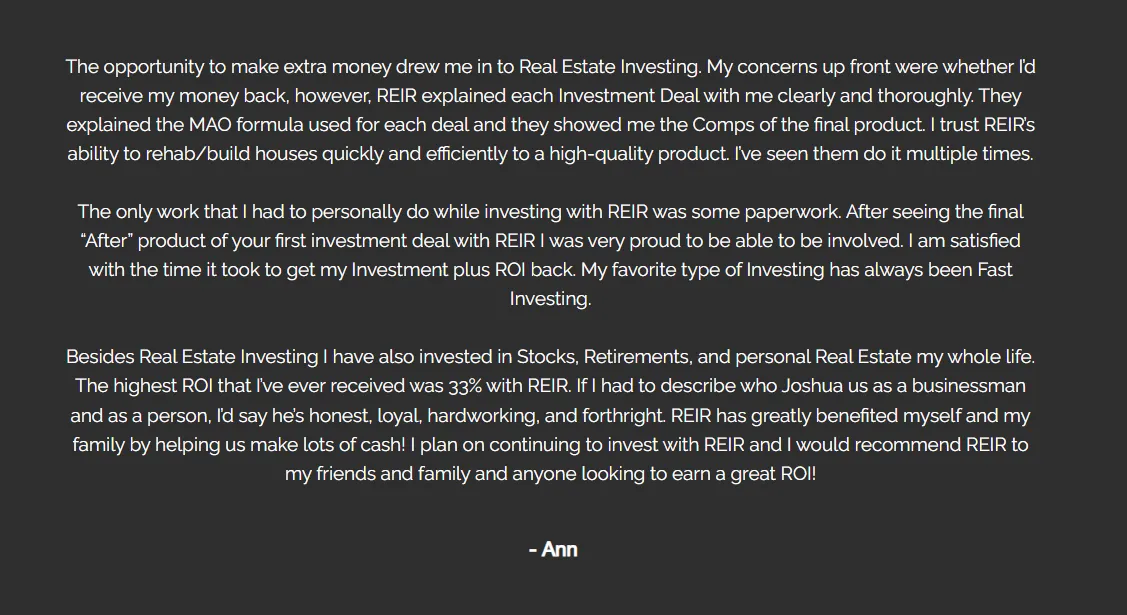

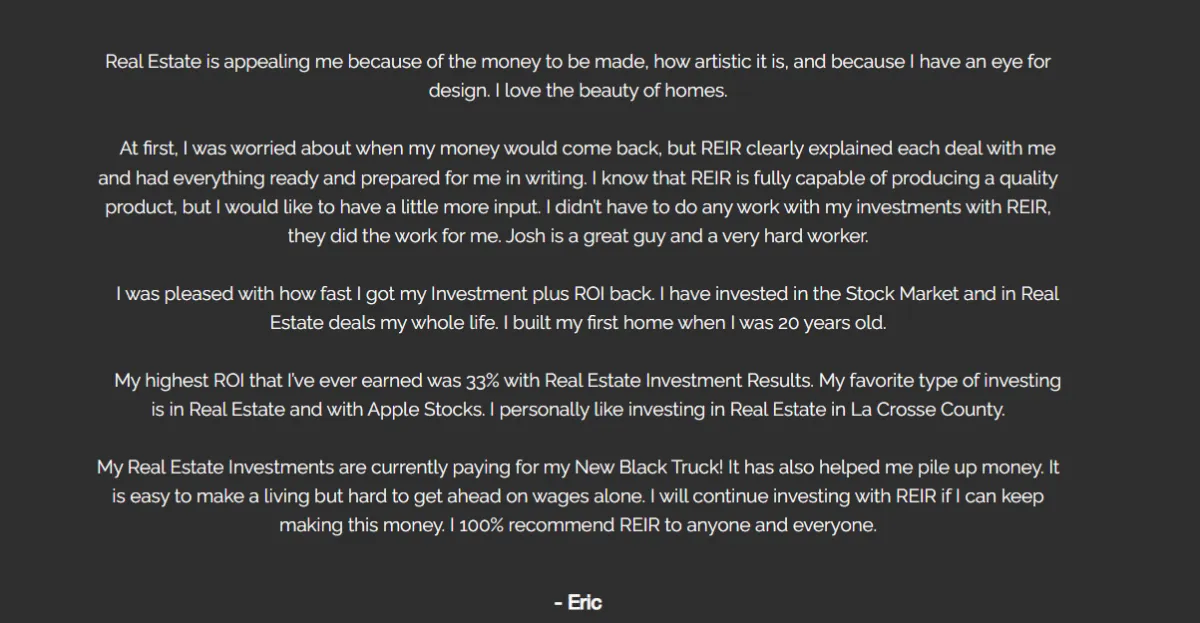

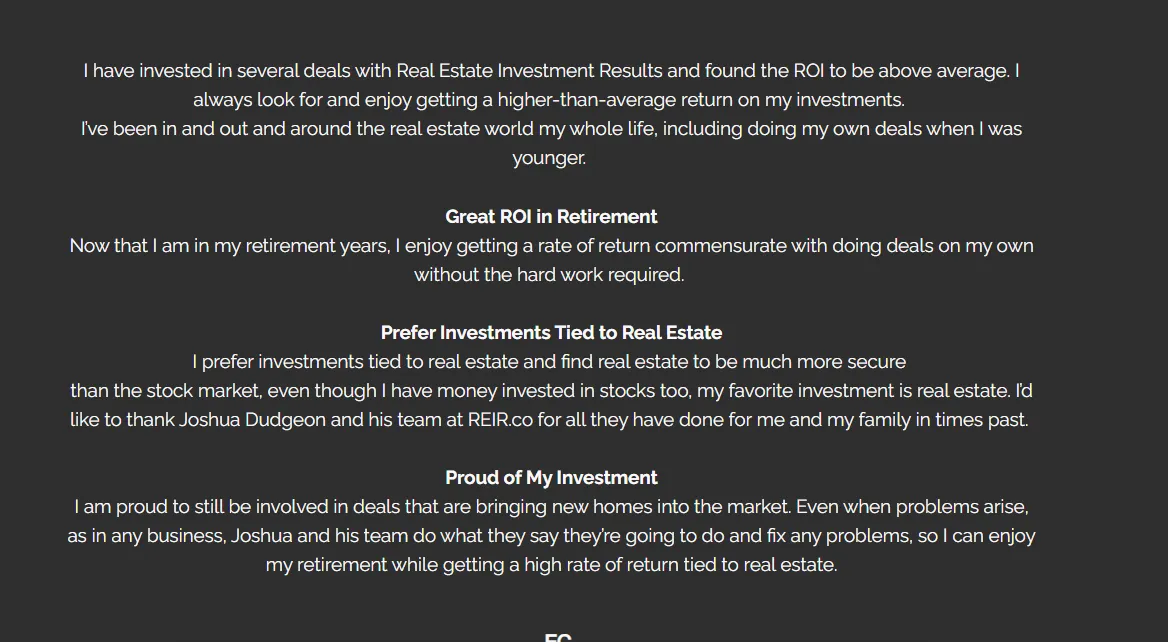

Testimonials

Blog

2025 Will Bring Big Changes to Real Estate Investing

The Rise of AI: A Game Changing Moment for Humanity

The Power of Perseverance Take the Next Step And Overcom

© 2026 by Real Estate Investment Results